Have you heard the news? THEY’RE ENGAGED!!!

That’s right, your social media teacher President Trump and economic policy teacher Lisa Cook are engaged in a political drama that shook markets on Tuesday.

Here’s how major asset classes performed in the latest trading sessions!

Headlines:

- Japan services producer prices index for July: 0.3% m/m vs. -0.2% m/m previous

- Australia RBA meeting minutes showed the recent rate cut was on a data-driven stance, citing inflation now within target and labor market easing. Further rate cuts may follow as global and domestic uncertainties persist

- US President Trump orders the removal of FOMC member Lisa Cook

- FOMC member Lisa Cook to legally challenge Trump’s dismissal

- France consumer confidence for August: 87.0 (88.0 forecast; 89.0 previous)

- BOE member Mann said keeping rates at the current level was ‘appropriate right now’ as sticky inflation persists

- Canada manufacturing sales prel for July: 1.8% m/m (0.1% m/m forecast; 0.3% m/m previous)

- US President Trump threatens tariffs on countries with digital taxes

- US President Trump Warns of 200% tariff on China if Beijing curbs rare-earth magnet exports

-

U.S. durable goods orders for July: -2.8% m/m (-2.5% m/m forecast; -9.3% m/m previous)

- Core durable goods orders was 1.1% m/m (-0.4% m/m forecast; 0.2% m/m previous)

- U.S. FOMC member Barkin said he sees little variation in economic activity over the rest of the year; sees potential for modest adjustment to interest rates

- U.S. house price index for June: -0.2% m/m (-0.1% m/m forecast; -0.2% m/m previous); 2.6% y/y (2.8% y/y previous)

- U.S. S&P/Case-Shiller home price for June: 2.1% y/y (2.7% y/y forecast; 2.8% y/y previous); 0.0% m/m (0.2% m/m forecast; 0.4% m/m previous)

- U.S. CB consumer confidence for August: 97.4 (96.0 forecast; 97.2 previous)

- U.S. Richmond Fed manufacturing index for August: -7.0 (-19.0 forecast; -20.0 previous)

- U.S. Dallas Fed services index for August: 6.8 (1.0 forecast; 2.0 previous)

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Traders started the day cautiously, keeping positions light ahead of Nvidia’s earnings and Friday’s US core PCE report. But the quiet mood didn’t last long. Trump’s unprecedented attempt to fire Fed Governor Cook grabbed the spotlight and rattled nerves, setting the tone for the rest of the session.

European stocks got hammered, with the Stoxx 600 sliding 0.83% and France’s CAC 40 plunging 1.7% as political uncertainty flared around Prime Minister Bayrou’s confidence vote. The selloff only deepened once Trump raised tariff threats, this time aimed at countries with digital taxes and at China’s rare earth exports.

Across the pond, U.S. markets managed to shake off the noise. The S&P 500 climbed 0.41% as traders spun Fed drama into a story of easier policy down the road. Safe-haven demand was alive and well, though, with gold pushing higher to $3,393 on Fed independence worries and a softer dollar. Oil wasn’t so lucky, WTI sinking 2.4% to $63.30 on trade war fears.

Bonds painted their own picture, the 10-year yield slipping 1.7 basis points to 4.26% while the curve steepened to 122 basis points, the widest since January 2022. Bitcoin, meanwhile, held just under $112,000 but couldn’t muster a breakout as flows stayed glued to safer ground.

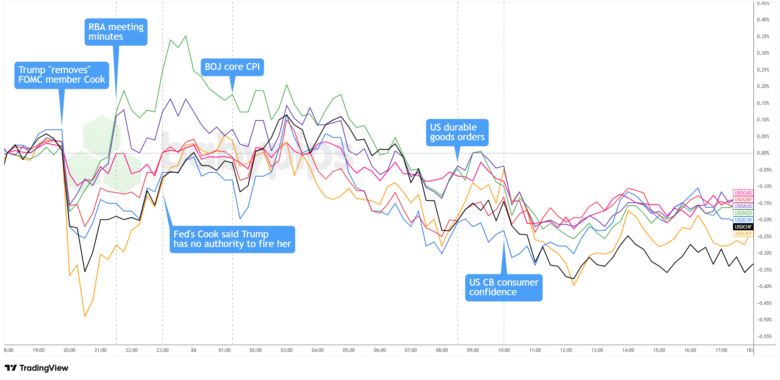

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Majors Chart by TradingView

The dollar started Tuesday with dramatic weakness, plunging after Trump’s social media announcement that he was firing Fed Governor Cook for alleged mortgage fraud. The Greenback tumbled against safe-haven currencies as gold surged, with the move reflecting immediate market fears about Fed independence and the potential for politically-driven monetary policy decisions that could undermine institutional credibility.

Asian session traders witnessed a partial recovery after Cook responded that Trump lacked authority to dismiss her and would challenge the action in court. However, the reprieve proved temporary as European markets opened to renewed dollar selling. Escalating tariff threats against digital tax countries and China over rare earth minerals compounded concerns about U.S. policy unpredictability and global trade stability.

The Greenback attempted a modest comeback during U.S. hours following better-than-expected durable goods orders, which fell only 2.8% versus the 4.0% forecast, while consumer confidence edged up to 97.4.

Despite these, the dollar closed broadly weaker against major counterparts. Safe-haven currencies remained firm throughout the session, with yen and Swiss franc outperforming as defensive flows persisted, underscoring deep anxiety about institutional integrity and the unprecedented nature of Trump’s Fed intervention.

Upcoming Potential Catalysts on the Economic Calendar

- Germany GfK consumer confidence for September at 6:00 am GMT

- Swiss economic sentiment index for August at 8:00 am GMT

- U.K. CBI distributive trades for August at 10:00 am GMT

- U.S. MBA mortgage applications for August 22, 2025, at 11:00 am GMT

- U.S. EIA crude oil stocks change for August 22, 2025, at 2:30 pm GMT

- U.S. Fed Barkin speech at 4:45 pm GMT

London trading should stay fairly muted with only second-tier European data on tap today, leaving traders cautious as they eye Nvidia’s earnings and the upcoming US core PCE release.

In New York, mortgage and oil stock data plus Fed speak could stir some price action, but overall volatility may stay limited while markets digest the Trump-Cook drama and wait for bigger catalysts.

As always, look out for global trade developments and geopolitical headlines that could influence overall market sentiment. Stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!