The Fed cut interest rates by 25bp as expected from 4.00% to 3.75% in their December decision, with policymakers signaling a higher bar for further easing.

This decision was reached through a 9-3 vote, with two hawkish members calling for no change in policy while dovish policymaker Miran favored a larger 50bp interest rate cut, marking the first time such a split happened since September 2019.

Key Takeaways

- Rate Cut Delivered: The FOMC lowered the target range for the federal funds rate by 25 basis points to 3.50-3.75%, marking the third consecutive reduction since September

- Hawkish Pivot in Projections: Updated Summary of Economic Projections showed the median “dot plot” now anticipates just two quarter-point cuts in 2025, down from four projected in September

- Inflation Concerns Elevated: The Committee acknowledged that inflation “has moved up since earlier in the year and remains somewhat elevated,” with PCE inflation projected at 2.9% for 2025 (up from 3.0% in September) before declining to 2.4% in 2026

- Labor Market Reassessment: The statement noted that “downside risks to employment rose in recent months,” though job gains have merely “slowed” rather than collapsed

- Dissent Signals Division: Three members dissented, as Stephen Miran preferred a 50bp cut, while Austan Goolsbee and Jeffrey Schmid preferred no change, highlighting internal debate over the appropriate pace of policy adjustment

- Balance Sheet Adjustments: The Fed announced it will begin purchasing shorter-term Treasury securities to maintain ample reserves as the balance sheet continues to normalize

The official statement acknowledged that “economic activity has been expanding at a moderate pace” but that “job gains have slowed” while inflation remains “somewhat elevated,” highlighting the delicate balancing act of the central bank as it navigates conflicting signals.

The three dissenting votes underscored this uncertainty. Miran’s preference for a larger cut highlights concerns about employment risks, while Goolsbee and Schmid’s preference for no cut emphasizes inflation concerns.

Link to FOMC Monetary Policy Statement (December 2025)

Meanwhile, the updated Summary of Economic Projections revealed a notable hawkish shift in the Committee’s outlook. GDP growth projections were revised higher to 2.3% for 2026 (from 1.8% in September) while the unemployment rate is expected to peak at 4.5% in 2025 before gradually declining to 4.2% by 2028.

More notably, the inflation outlook remains stubbornly elevated. Core PCE inflation is projected at 3.0% for 2025 before moderating to 2.5% in 2026,with both figures suggesting inflation may remain above the Fed’s 2% target for an extended period.

Link to FOMC Summary of Economic Projections (December 2025)

The dot plot forecasts indicated that the median federal funds rate projection for end-2025 rose to 3.6% (implying two cuts from the current 3.625% midpoint), compared to the September projection of 3.4% (which would have implied four cuts).

For 2026 and 2027, the median remains at 3.4% and 3.1% respectively, suggesting a slower and more measured approach to reaching the long-run neutral rate of 3.0%.

During the press conference, Fed Chairperson Jerome Powell emphasized that the Committee is now approaching or possibly at the point where it would be appropriate to slow the pace of rate cuts.

He stressed that future decisions would be “meeting by meeting” and heavily data-dependent, with no preset course of action. Powell also reiterated that with policy now “significantly less restrictive” than it was, the FOMC can afford to be more cautious in considering further adjustments.

Link to Fed Chairperson Powell’s Press Conference (December 2025)

Regarding the labor market, Powell described current conditions as “solid” rather than weak, with the unemployment rate still relatively low by historical standards. He suggested that much of the recent uptick in unemployment reflected increased labor supply rather than significant job losses.

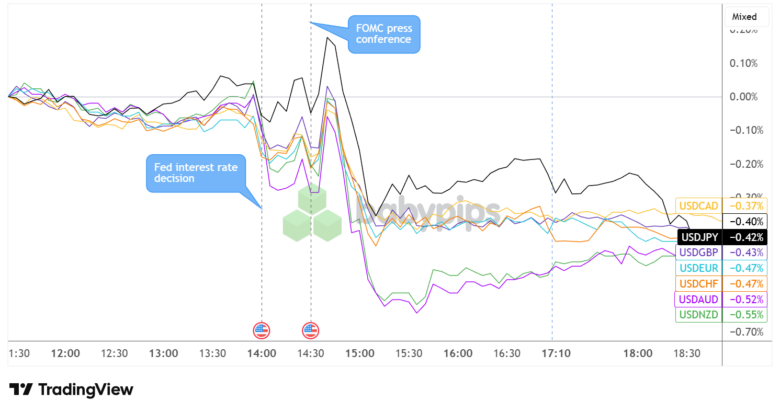

Market Reactions

U.S. Dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar, which had been consolidating ahead of the FOMC decision, broke lower across the board when the Fed delivered the anticipated 0.25% interest rate cut. A bit of risk-taking also appeared to kick in and weigh on the Greenback thanks to upgraded growth forecasts in the quarterly Summary of Projections.

USD leveled off from its post-FOMC drop as traders braced for Fed head Powell’s press conference, which then led to a brief rally for the currency on confirmation of more cautious easing decisions up ahead.

However, the dollar’s post-presser gains were short-lived, as it staged a more prolonged selloff that lasted roughly an hour after the event. The currency eventually stalled from its drop and pulled slightly higher as profit-taking followed until the end of U.S. market hours, before another bearish wave appeared to take place early in the next session.