It was another messy day in the financial markets, as asset classes took cues from their own individual catalysts.

Gold struck a fresh record high while global uncertainties lingered while crude oil rebounded thanks to new U.S. sanctions on Iran and China.

Major currencies also had plenty to work with, including a couple of top-tier jobs releases and major central bank announcements.

Here are the latest headlines and economic reports you need to know.

Headlines:

- China held its benchmark rate steady for the fifth straight month, with the one-year loan prime rate at 3.1% and five-year LPR at 3.6%

- Australia Employment Change for February 2025: -52.8k (35.0k forecast; 44.0k previous); Unemployment Rate for February 2025: 4.1% (4.1% forecast; 4.1% previous)

- Swiss Balance of Trade for February 2025: 4.3B (3.9B forecast; 4.0B previous)

- Germany PPI for February 2025: -0.2% m/m (0.1% m/m forecast; -0.1% m/m previous); 0.7% y/y (1.0% y/y forecast; 0.5% y/y previous)

- U.K. Claimant Count Change for February 2025: 44.2k (15.0k forecast; 22.0k previous); unemployment Rate for January 2025: 4.4% (4.4% forecast; 4.4% previous); Average Earnings excl. Bonus (3Mo/Yr) for January 2025: 5.9% (5.9% forecast; 5.9% previous)

- SNB cut interest rates from 0.50% to 0.25% as expected, its lowest level since 2022 to deter inflows to franc

- Euro area Construction Output YoY for January 2025: 0.0% (0.2% forecast; -0.1% previous)

- BOE kept interest rates on hold at 4.50% as expected in 8-1 MPC decision (7-2 forecast)

- During the BOE press conference, BOE Governor Bailey urged caution about a turbulent global backdrop and uncertain effects on inflation and growth

- Canada PPI for February 2025: 4.9% y/y (5.0% y/y forecast; 5.8% y/y previous)

- Canada Raw Materials Prices for February 2025: 9.3% y/y (10.1% y/y forecast; 11.8% y/y previous); 0.3% m/m (0.5% m/m forecast; 3.7% m/m previous)

- U.S. Initial Jobless Claims for March 15, 2025: 223.0k (225.0k forecast; 220.0k previous)

- U.S. Philadelphia Fed Manufacturing Index for March 2025: 12.5 (11.0 forecast; 18.1 previous)

- U.S. announced new oil sanctions on Iran tankers and China’s “teapot” refineries

- U.S. Current Account for December 31, 2024: -303.9B (-340.0B forecast; -310.9B previous)

- U.S. Existing Home Sales for February 2025: 4.2% m/m (-0.7% m/m forecast; -4.9% m/m previous)

- U.S. President Trump refrained from making any promises regarding strategic crypto reserve during the Digital Asset Summit in NY

Broad Market Price Action:

Dollar Index, Gold, SP 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Price action during the Asian and London sessions showed a bit of calm after the FOMC storm, as asset classes settled in ranges and braced for the next round of major catalysts.

Gold held its ground in positive territory, touching fresh all-time highs near $3,057 before profit-taking and dollar strength dragged it back down as the London session went on.

WTI crude oil also kept its head afloat, eventually surging to $68.40 after the U.S. imposed new sanctions on Iran’s oil tankers and China’s “teapot” refineries, triggering another set of global supply concerns.

Bitcoin also started off on solid footing but retreated from $87,200 to $84,273, as investors seemed disappointed when Trump made no policy promises during his appearance at the Digital Asset Summit in New York.

Global equities struggled to find direction, with European markets reeling from global growth concerns. Germany’s DAX slipped 1.18% and Italy’s FTSE MIB tumbled 1.32% while the U.K. FTSE 100 showed relative resilience with a meager 0.05% loss for the day.

U.S. equities had a choppier run, initially attempting to extend the post-FOMC risk rally before caving in to bearish pressure. The S&P 500 closed down 0.22% at 5,662.89, the NASDAQ shed 0.33% to 17,691.63, and the Dow Jones Industrial Average ended marginally lower by 0.03% at 41,953.32.

Treasury yields ended the day marginally lower across most of the curve, with the benchmark 10-year yield dipping 1.5 basis points to 4.24% after economic data provided mixed signals on the U.S. economy’s health.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

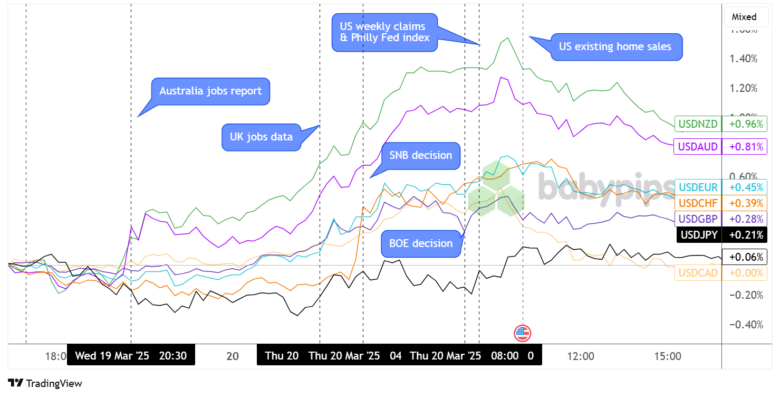

The Greenback was still shaking off the post-FOMC bearish vibes, before it staged a sharp rally versus the Aussie and Kiwi on weaker than expected jobs data from the Land Down Under. Other major currencies fought to stay afloat versus the dollar but eventually gave in to broader risk aversion, as global growth uncertainties weighed on European markets.

It didn’t help that the U.K. also printed mostly downbeat jobs figures, further stoking the weakening growth narrative. The SNB cut interest rates as expected in an effort to discourage more inflows to the safe-haven franc, triggering a sharp pop higher for USD/CHF as well.

Later in the London session, the BOE announced its decision to keep interest rates on hold, even surprising with a less dovish MPC vote as only one member called for an easing move this time. Sterling briefly scored gains during the announcement but resumed its slump versus the dollar, with GBP/USD closing 0.28% lower for the day.

Although the yen put up a pretty strong fight versus the U.S. dollar for the most part of the day, with the Japanese currency also benefitting from risk-off flows and anti-USD sentiment, it was the Canadian dollar that proved most resilient as USD/CAD closed flat with the Loonie getting a boost from higher oil prices.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. Public Sector Net Borrowing at 7:00 am GMT

- Germany Bundesbank Mauderer Speech at 9:00 am GMT

- Euro area Current Account for January 2025 at 9:00 am GMT

- U.K. CBI Industrial Trends Orders for March 2025 at 11:00 am GMT

- Canada Headline and Core Retail Sales at 12:30 pm GMT

- Canada New Housing Price Index for February 2025 at 12:30 pm GMT

- U.S. Fed official Williams Speech at 1:05 pm GMT

- Euro area Consumer Confidence Flash for March 2025 at 3:00 pm GMT

The economic schedule appears a bit lighter compared to the previous trading sessions since the only top-tier data point due is Canada’s retail sales report for February.

Still, keep your eyes and ears peeled for geopolitical headlines and tariffs updates that could impact overall market sentiment.

Don’t forget to check out our brand new Forex Correlation Calculator when taking any trades!