JPow shook the markets on Thursday when he hinted that the FOMC gang isn’t in any hurry to cut interest rates further.

How did the major assets react to the possibility?

We’re breaking down the biggest market movers in the last trading sessions!

Headlines:

- RBA Gov. Bullock thinks the central bank is “restrictive enough” and will remain restrictive until they’re confident in the “downward trajectory in demand”

- RICS: U.K. house price growth appears to be “gradually gaining momentum” though the rise in bond yields may present headwinds

- Euro Area flash employment change maintained a 0.2% q/q uptick as expected in Q3

- Euro Area flash GDP saw another 0.4% q/q increase in Q3 as expected

- Euro Area industrial production dropped by 2.0% m/m in September after a 1.5% increase in August

- FOMC voting member Adriana Kugler favors keeping rates steady “if inflation doesn’t retreat further” but is open to gradually cutting rates “if the labor market slows down suddenly”

- U.S. PPI for October: 0.3% m/m as expected (0.2% previous); Core PPI accelerated from 0.1% to 0.2% as expected

- U.S. initial jobless claims for the week ending Nov 9: 217K (224K expected, 221K previous)

- EIA: U.S. crude oil inventories jumped by 2.1M barrels in the week ending Nov 8 (+0.4M expected, +2.1M previous)

- Fed Chairman Powell said “The economy is not sending any signals that we need to be in a hurry to lower rates,” giving them the “ability to approach our decisions carefully.“

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The U.S. dollar kept a strong hold over major assets yesterday, boosted by expectations of higher deficit spending and persistent U.S. CPI and PPI data, which have cooled hopes for near-term Fed rate cuts.

JPow added to the cautious sentiment, remarking that “The economy is not sending any signals that we need to be in a hurry to lower rates.” This came just after other FOMC members signaled a more gradual approach to easing, putting a damper on risk-taking.

While European stocks managed a slight rebound from trade war jitters, U.S. indices all edged lower, weighed down by shrinking prospects for further Fed rate cuts. The CME FedWatch tool now shows just a 59.1% chance of a 25-bps rate cut in December, down from 85% earlier this week.

The dollar’s extended rally pressured gold for a fifth straight session—the metal’s longest losing streak in nine months. Gold did get a lift from its dip near $2,540, ending the day just under $2,570. Bitcoin, too, saw more pullback, sliding down to $87,500 after recently testing $91,500.

Meanwhile, WTI crude oil found support around $68.00, briefly touching $69.30 before closing near $68.50. This came despite the International Energy Agency (IEA) forecasting a demand-supply imbalance by 2025 and the U.S. Energy Information Administration (EIA) reporting a bigger-than-expected inventory buildup.

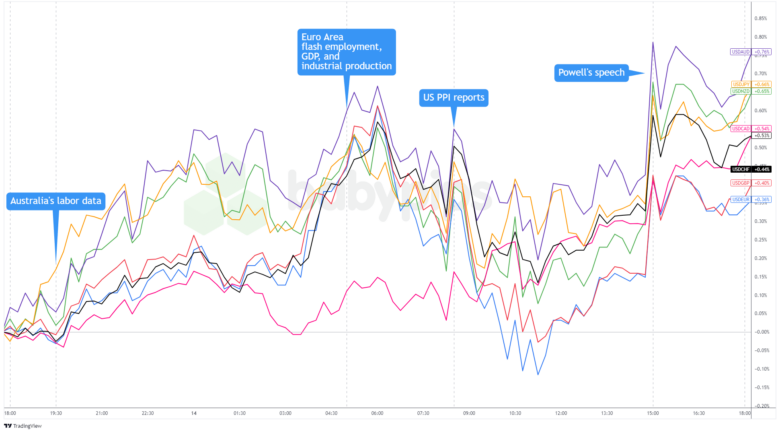

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar kicked off the day with strength, still fueled by post-election trends. The Greenback even gained more ground after the the Euro Area printed relatively strong GDP and employment numbers but also weak industrial production data. USD/CAD was an exception, likely due to CAD receiving a bump from higher crude oil prices.

The dollar gave back some gains just before the U.S. session, as traders likely took profits ahead of the PPI report. Sticky-high PPI numbers initially lifted the dollar, though uncertainty around the Fed’s December policy decision brought it closer to its open prices.

Later in the day, Fed Chair Powell took the stage, signaling that the Fed isn’t in a rush to cut rates further. This statement gave the dollar fresh momentum, pushing it 0.30% to 0.70% higher against most major currencies.

Upcoming Potential Catalysts on the Economic Calendar:

- Germany wholesale prices at 7:00 am GMT

- U.K. GDP (m/m) at 7:00 am GMT

- U.K. preliminary GDP (q/q) at 7:00 am GMT

- U.K. goods trade balance at 7:00 am GMT

- U.K. services index at 7:00 am GMT

- U.K. industrial and manufacturing production at 7:00 am GMT

- Switzerland PPI at 7:30 am GMT

- France final CPI at 7:45 am GMT

- EU economic forecasts at 10:00 am GMT

- Canada manufacturing and wholesale sales at 1:30 pm GMT

- U.S. retail sales reports at 1:30 pm GMT

- U.S. NY manufacturing index at 1:30 pm GMT

- U.S. import prices at 1:30 pm GMT

- FOMC member Collins to give a speech at 2:00 pm GMT

- U.S. industrial production at 2:15 pm GMT

- U.S. business inventories at 3:00 pm GMT

- Australia CB leading index at 3:30 pm GMT

- FOMC Member Williams to give a speech at 6:15 pm GMT

We’ll see another data parade in the next few sessions, with European traders likely focusing on the U.K.’s GDP data and business investment figures, which could signal the strength of the British economy and impact the pound.

In the U.S., retail sales and industrial production numbers, alongside speeches from FOMC members, may offer insight into consumer demand and the Fed’s stance and influence the dollar’s direction for the rest of the day.

Keep an eye out for any major surprises, as well as potential shifts in central bank rhetoric, that could steer the U.S. currency in a strong direction and don’t forget to check our new Currency Correlation tool when taking any trades!